Can Financial Services Be More Than Money? Transforming Baby Boomer Retirement Planning into Longevity Planning

Earlier this month Bank of America Merrill Lynch produced a webcast on “Health Care in Retirement”. Thewebcast was part of Bank of America Merrill Lynch’s Help2Retire webcast series.I was pleased to be invited by Merrill Lynch to participate with a great panelof discussants.

View webcast (click here)

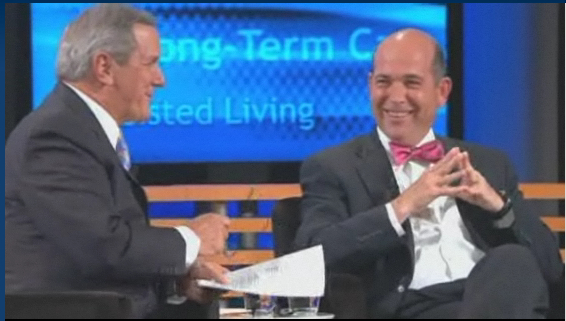

(left to right) Charles Gibson, Joseph Coughlin,

Diana Nyad, Jacob Hacker & Andrew Sieg

Hosted before a livestudio audience by former ABC News Anchor Charles Gibson, the roundtableincluded Merrill Lynch’s Andrew Sieg, Head of Retirement & PhilanthropicServices; Jacob Hacker, Professor of Political Science, Yale University andauthor of the new book Health Care forAmerica; and, world-renowned long-distance swimmer, sports journalist andfitness expert Diana Nyad.

The panel made many observations on the impact of health care onretirement planning and savings. Merrill Lynch’s Andrew Sieg advised consumersto discuss future health care expenses and the strategies to meet those costswith their financial advisor. Professor Hacker provided insight into therecently passed national health care policy and its implications for futureretirees. Diana Nyad pushed everyone as a good coach might push a star athleteto invest in their physical health as much as they plan for their financialsecurity.

From Retirement Planning to Longevity Planning

While the discussion was framed around health care andretirement, clearly a critical part of later life, Iurged clients and financial services to use this as an opportunity to think beyond classic retirement planning. Instead, we should transform financial planningfor later life into longevity planning. Whatwill you be doing in older age and how will you pay for those activities,services and needs? Rather than adapting old metaphors about accumulation andtools to measure financial progress, what might be the new consumer realitiesand business opportunities for planning to live longer?

Here are three:

Caregiving: According tothe Gallup-Healthways Well-Being Index, at least one in four American familiesprovide care to a loved one. In fact, the Gallup-Healthways data shows that onaverage these families invest ~21 hours per week providing a range of mundaneto intense services.(see Estimating the Impact of Caregiving and Employment on Well-Being)

Caring has its costs.Beyond the tax on personal well-being, there are financial costs. A MerrillLynch study conducted earlier this year showed that nearly one-third ofaffluent clients with investable assets of $250,000 or more were redirectingsome of their resources from savings or even a child’s college fund to financecaregiving needs. Genworth released the results of a nationwide survey (October12, 2010) indicating that more than 70 percent of consumers providing directcare to a loved one reduced their savings contributions. Other researchconducted by AARP, MetLife and the National Alliance of Caregiving indicatesthat plans to work longer to improve financial security into old age may behampered by the need to provide care to a frail parent or spouse.

Health & Well-Being: The saying goes ‘ifyou have your health, you have everything.’ Well, maybe, but it will cost you.Fidelity Investments suggests that healthcare may cost a couple over 65 morethan $250,000 in out-of-pocket expenses – not including nursing home expenses.This translates into more than $500.00 per month for the average Americancouple.

Moreover, as we livelonger we will be more likely to be managing one or more chronic diseases. Thecost burden of chronic disease impacts out-of-pocket expenses that are oftenwell beyond private and public health insurers. These may include purchases forspecial dietary needs, devices to monitor everything from blood glucose toblood pressure or other services that support quality of life while insurancepays for treatment of the disease. The next discussion with a financial advisormay include the usual – financial goals, income, portfolio risk distribution andwhat were the results of your last check-up?

Aging-in-Place: In betweenthe twin bookends of retirement – healthcare and finance, there is thepractical often unspoken reality of where to live and how to stay there. Mostretirees do not move to a desert golf course or a beachfront community. By thetime 50 years old rolls around, the vast majority of people choose toage-in-place in the home they know and love.

What does aging-in-placecost? Routine home maintenance may become more important as the home you havelived in for decades ages with you. As you age, the desire or the capacity tostand on a high ladder to fix gutters or change light bulbs may becomeproblematic. If driving becomes difficult, how will transportation be arrangedto maintain connections with all the things that make up life?

Services are emerging.Home maintenance services for homeowners too busy or too overwhelmed are nowserving older adults and distant caregivers. Beacon Hill Village is acooperative network of neighbors in Boston’s Beacon Hill neighborhood thatcontracts out for services that includes everything from home maintenance, housekeeping,grocery delivery, transportation, to entertainment. If your two-story homebecomes a challenge to your creaky knees what will it costs to install anelevator, a chair lift or to convert a first floor room into a bedroom? All ofthese services and needs are out-of-pocket expenses. They may not be part of aretirement dream, but they are part of living longer.

Longevity Planning andInnovations in Financial Services Consumer Engagement

These are only three dimensions of ‘longevity thinking’, not ‘retirementplanning’. Retirement, as currently presented by financial product developers,wholesalers and advisors is still about accumulation and smart spending. Notincorrect, but incomplete. Developing new products, services and advice tosupport longevity will get the baby boomer’s attention, engage them in adiscussion that is both rational and emotional, and persuade them to takesustained action.